When we think of China, what comes upper most in our mind in the textile and clothing sector is its dominance over the global apparel trade. It currently holds a share of 35 per cent in this segment compared to India’s just 5 per cent. China’s share is expected to come down due to domestic pull in demand. What is more, China has already ventured into the manufacturing of high end man-made fabric based textiles and apparel to grab a big share in the global market. On the other hand, India is mostly cotton based textiles for export and its presence in the synthetic segment in the global market is insignificant.

China, Taiwan and other countries are into the business of synthetic textiles manufacturing, looking at the global trends. Synthetic is projected to be the fibre of the future. It is expected to cover around 60 per cent of the total fibre demand globally, while cotton is to account for a onefourths share by 2030. All this is because of the “Drastic shift in the global textiles and apparel industry from cotton to synthetic,” says Sanjay Arora, Business Director, Wazir Advisers Pvt Ltd. “Why synthetic? It is because of its cost effectiveness. It is a fibre that can be blended with other fibres like cotton and spandex for performance requirements. Again, recycled polyester have achieved a “pride of place as a green textile option today,” opines Arora.

Currently, if you look at the global fibre demand, cotton accounts for 26 per cent and polyester 56 per cent. In 2007 this share was about 35 per cent for both. The popularity of synthetic textiles has been rising rapidly. This is because of lowcost, demand supply gap in cotton and versatility design and application. For instance, global cotton supply is not increasing in line with the overall fibre demand growth, with fibre demand increasing due to rise in population and consumer prosperity in developing countries. However, the land under cotton cultivation is decreasing due to competing land use which is more attractive.

The MMF industry is largely polyester dominated which constitutes about 82 per cent of its total production. There is vast scope for increasing consumption of MMFs in the country, since the share of MMF products in total textile production is considerably lower than the world average. Infact, the share of MMF products in exports is even lower than that of total textile production. Globally, India ranks second in man –made filament yarn production. It has a 12 per cent share of global production of cellulosic fibre and filament and 7 per cent in synthetic fibres and filaments.

There is a myth in the textile industry that polyester is for the rich and cotton for the poor. Therefore, tax polyester based products at a higher rate. Nothing can be farther from the truth. The fact is that it is the less-wealthy sections of society, which wear polyester because of the lower cost of maintenance and longer life, says the Rahul Mehta, President, Clothing Manufacturers Association of India.

Cotton is favoured by the rich who do not mind the shorter life and higher cost of maintenance. CMAI wants the fibre disparity in GST rates across the value chain to be removed, though there is full neutrality at the apparel stage. He also touched upon the differential rates between apparels of below and above Rs. 1,000 in the present situation to say that a garment worth Rs. 1,200 or Rs. 1,500 is worn only by the rich is strange. India has become aspirational and exposure to the Internet and TV has raised expectations of consumers. They are beginning to realize the value of brands. In such a scenario, to charge 7 per cent extra on goods above Rs. 1,000/- is unnecessarily curbing consumption and “encouraging manufacturers to cut corners to keep their prices below the threshold level.”

The textiles and clothing sector has a special place in the Indian economy in terms of its contribution to output, exports and job creation. It contributes about 4 per cent of GDP and about 10 per cent of exports. It is the largest employer after agriculture. It has the ability to provide employment to the people at the bottom of skill pyramid. It is also attractive to high skilled engineers, designers and other professionals.

The industry caters to the basic need of the people, i.e. clothing for wearing and various other usages. With a population of 1.3 bn people, the clothing consumption will grow, creating domestic demand for textiles products. Currently, per capita consumption is about 5 kg against the world average of 13.5 kg and China’s 16 kg. Thus shows the potential for growth.

The industry caters to the basic need of the people, i.e. clothing for wearing and various other usages. With a population of 1.3 bn people, the clothing consumption will grow, creating domestic demand for textiles products. Currently, per capita consumption is about 5 kg against the world average of 13.5 kg and China’s 16 kg. Thus shows the potential for growth.

On the need for Indian textiles and clothing industry for diversifying into the high value synthetic segment, there is one more major reason. The country may witness saturated levels in the textile value chain (barring value addition). This underscores the need for the sector to emerge globally competitive in the synthetic segment across the value chain. In the absence it will be a far cry to achieve the projected textile business size of Rs. 350 bn from the current Rs. 208 bn and creation of 22 mm new jobs by 2025.

Already, the industry is suffering several disadvantages at home – 23 per cent to 30 per cent expensive synthetic raw materials, high interest and power costs. The industry also faces a 9.6 per cent to 20 per cent import duty in the global market and free trade agreements with neighbouring countries such as Bangladesh.

On GST, the Confederation of the Indian Textiles Industry (CITI) wants the tax on MMF yarnto be further reduced to 5 per cent from 12 per cent. Fabrics on the other hand attract GST at 5 per cent. This means the raw materials are charged more than the outputs, that is, fabrics. This leads to an inverted duty structure, leading to blockage of working capital etc. The reason advanced by CITI in seeking redirection of GST on MMF fibres from 18 per cent to 12 per cent is that it will provide jobs. These fibres are used by the spinning sector to produce yarn of special characteristics, unlike filament yarn which is directly produced by MMF manufacturers and fetches higher value addition.

It is also necessary to take safeguard measures to protect the domestic industry from cheaper imports of yarn and fabrics from neighbouring countries and China. The steps should include raising the import duty or levying additional customs duty on these two items. Again the rules of origin, including yarn and fibre forward rule, should be imposed on imports.

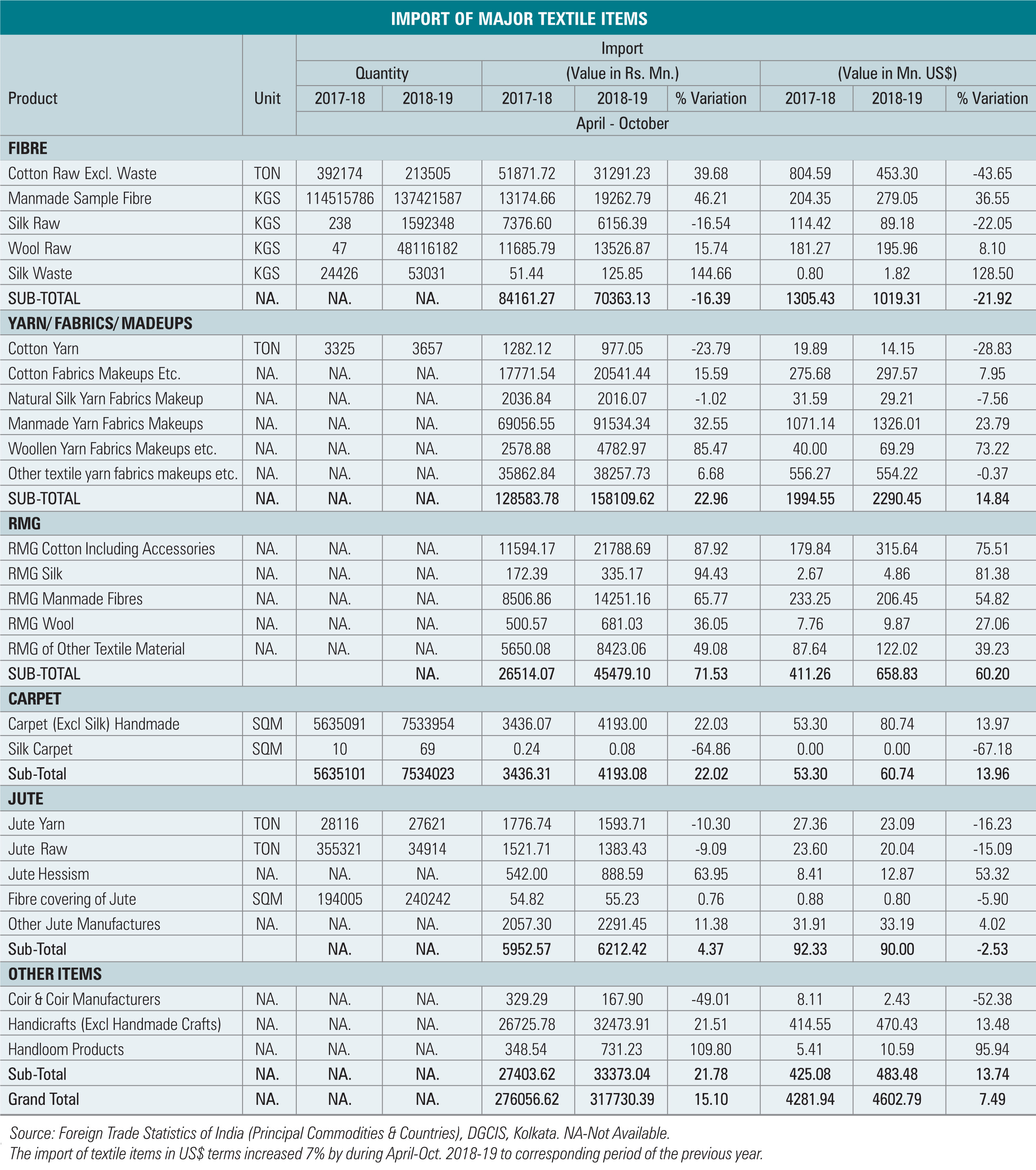

On the positive side, the government had, last year, doubled import duties on 196 man-made fabric categories to 20 per cent from the existing 10 per cent. The move was intended to safeguard the interest of domestic fabric manufacturers and attract investments in thesector. The import value of the products was around Rs. 900 mn in 2017- 18, up 62 per cent from 2016-17.

Many Indian players have recently announced expansions in the synthetic segments. “India’s largest textiles and apparel giant, Arvind, has recently added polyester knitted fabric to its portfolio and currently offering 100 per cent polyester poly spandex etc.,” says Arora. Moreover, a majority of the textile players are orienting themselves to synthetic fibre – based active wear /sportswear and performance wear fabrics.

Again, Bhilosa, Mumbai, which is a major polyester texturized yarn, is planning to double its capacity to produce 3,000 tonne per day in the near future. Gimatex Industries, also of Mumbai, has added Tencel model and cotton model yarns in its product offerings.

Against this encouraging scenario, opportunities in the polyester sector are huge for Indian manufacturers. On the production and export fronts, the picture is not encouraging. India’s MMF output rose marginally to 1,319 mn kg in 2017-18 up 0.2 per cent CAGR from 1,307 mn kg in 2013-14. MMF filament also declined at a CAGR rate of two per cent during the same period to reach 1,187 mn kg in 2017-18.

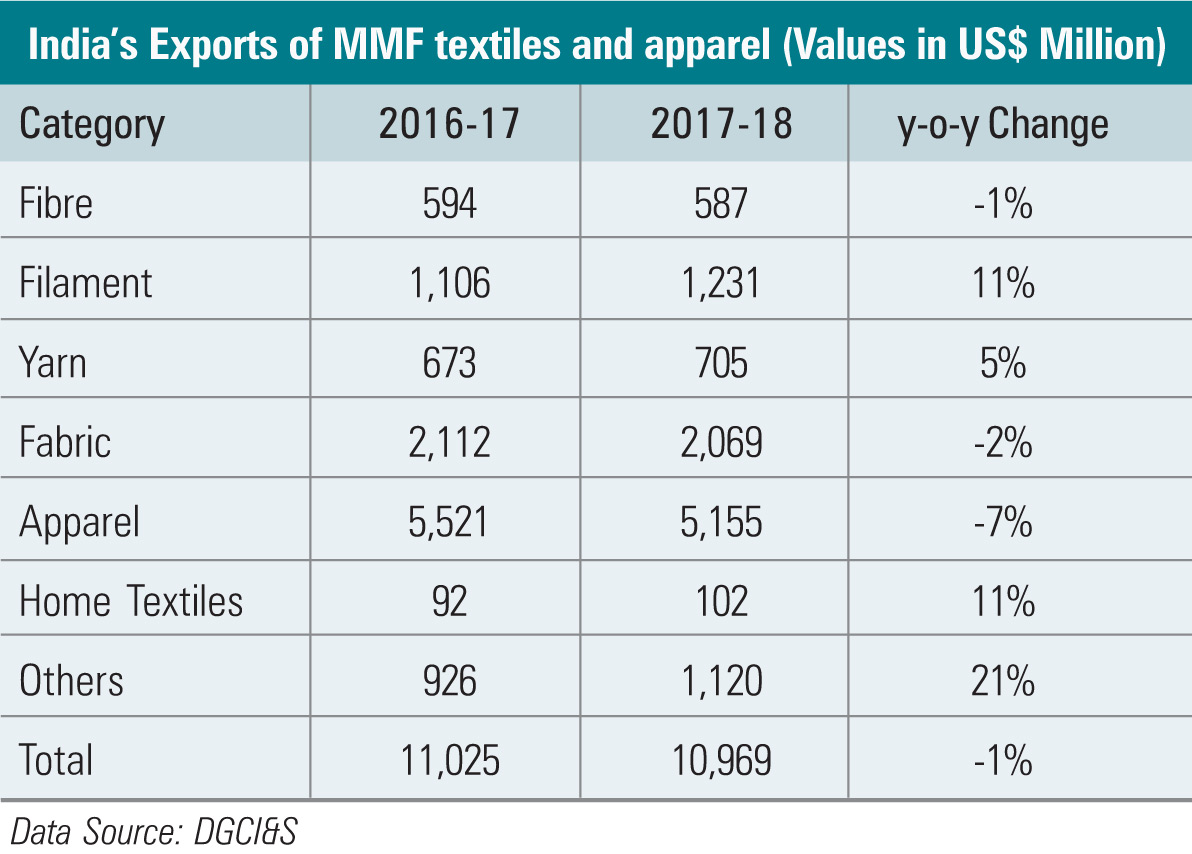

Exports of MMF based textiles and apparel fell from $11,025 mn in 2016-17 to $10,969mn in 2017-18, a one per cent decline. Exports of filaments, yarn and home textiles declined by one per cent, two per cent and 7 per cent respectively during the same period. Apparel contributes to a maximum share of 47 per cent followed by fabric (19 per cent) filament (11 per cent) yarn (6 per cent) and home textiles (one per cent).

{kind=link}