The Indian textiles and clothing (T&C) industry continues to be dogged by one problem or another. Ready-made garments exports in the 2019-20 fiscal saw a fall in June and a negative growth in August compared to the same months of last year. Reimbursement of dues to the industry as promised by the government are yet to be made. There is stiff competition in the global market. Added to that is the US trade war with China. Despite these, bigwigs in the industry in the South – mill owners, spinners, technocrats and human resources managers – have not given up hope. Opinion is veering round the view that closing down of establishments would not arise even if the situation turns worse in the coming months.

The industry is largely dependent on exports. It would therefore be necessary to take “corrective” action as foreign companies have been looking “inward”. That is what the industry must plead with the government, and there is no cribbing of the problem of competition from countries such as Bangladesh. The industry has to increase its efficiency and upgrade its units as successful companies have done so.

Again, the industry should not wait for the government to “do something”. What must be done is to cut down costs. It is to be noted that those who are close to customers or brand owners earn more profit. S Dinakaran former SIMA Chairman felt that “We have to change ourselves” while speaking at a SIMA Texpin 2019 held in Coimbatore recently. It coincided with the 12th CEO conference.

Stating that the ease of doing business had started showing improvements, KV Ramanand, Partner, Ernst and Young, sounded a note of warning that there had been no Initial Public Offers (IPOs) or even rights issues in the textile sector for some time. Also, there were no large financial transactions.

Speaking on “Disruptive Technology and HR Challenges” NK Ranganath said that the culture prevailing in the textile industry did not allow it to be “productive” and “quality consistent.” Impart training to people for future skills and not to lose sight of human touch. He wanted companies to invest on the well-being of their employees. Calculated risks could be taken after evaluating them. Besides, a “critical” look at processing is called for.

Dr. C Ramanandana, Senior General Manager Lakshmi Machine Works Ltd. said that there was “volatility” in the raw material prices. Raw materials accounted for about 50-55 per cent of the total cost, which exerted pressure on the spinning mills. A one per cent saving in power cost by using the existing technology could change the operational efficiency of the mills.

Dr. C Ramanandana, Senior General Manager Lakshmi Machine Works Ltd. said that there was “volatility” in the raw material prices. Raw materials accounted for about 50-55 per cent of the total cost, which exerted pressure on the spinning mills. A one per cent saving in power cost by using the existing technology could change the operational efficiency of the mills.

Durai Palanisamy, Managing Director, Pallava Textiles (P Ltd.) said the industry had to go a long way before it was able to utilize more of man-made fibre items or blends in manufacturing textiles and become competitive in the global market. Globally, about 70 per cent of fibre consumption is MMF. Opposite is the case in India where cotton consumption is around 80 per cent.

On cotton, K Sivaraj, Managing Director, Sivaraj Spinning Mills (P) Ltd. said there was a surplus in the country. The problem was holding stocks for more than six months. There was need to come up with a strategy with less investment for holding stocks.

Senthilnathan, Executive Chairman, Acsen Tax P. Ltd. touched upon the cotton yield gap between India and other countries. He claimed that India had the best seeds – 40 plus quintal per hectare in Maharashtra. Proper irrigation facilities could boost production yield. “We have to create hybrids to face pests.” There was no limit to increasing the yield and new yield technology was adopted in the US and Australia.

Senthilnathan, Executive Chairman, Acsen Tax P. Ltd. touched upon the cotton yield gap between India and other countries. He claimed that India had the best seeds – 40 plus quintal per hectare in Maharashtra. Proper irrigation facilities could boost production yield. “We have to create hybrids to face pests.” There was no limit to increasing the yield and new yield technology was adopted in the US and Australia.

Kiran Ranjit Soundarajan, Managing Director Soundarajan Mills Ltd, indicated that next year’s (2009-10) cotton crop would yield around 370 lakh bales compared to 343 lakh bales anticipated in the 2018-19 season. But domestic prices would continue to be high and mills would have to look at options in the market. In this situation, the government’s Minimum Support Scheme (MSP) would play a key role and Cotton Corporation of India (CCI) would commence its operations. In fact good cotton crops were also expected in other countries. With MSP prices likely to be higher than those prevailing globally, imports would be an attractive proposition. At the same time, he sought to strike a positive note. The domestic market was growing and the per capita consumption was also growing every year. R Elango, Managing Director, Sangeeth Textiles Ltd. noted that there was recession in some segments. Globally there was recession in the textile sector. There was excess supply in the spinning sector, leading to a fall in demand.

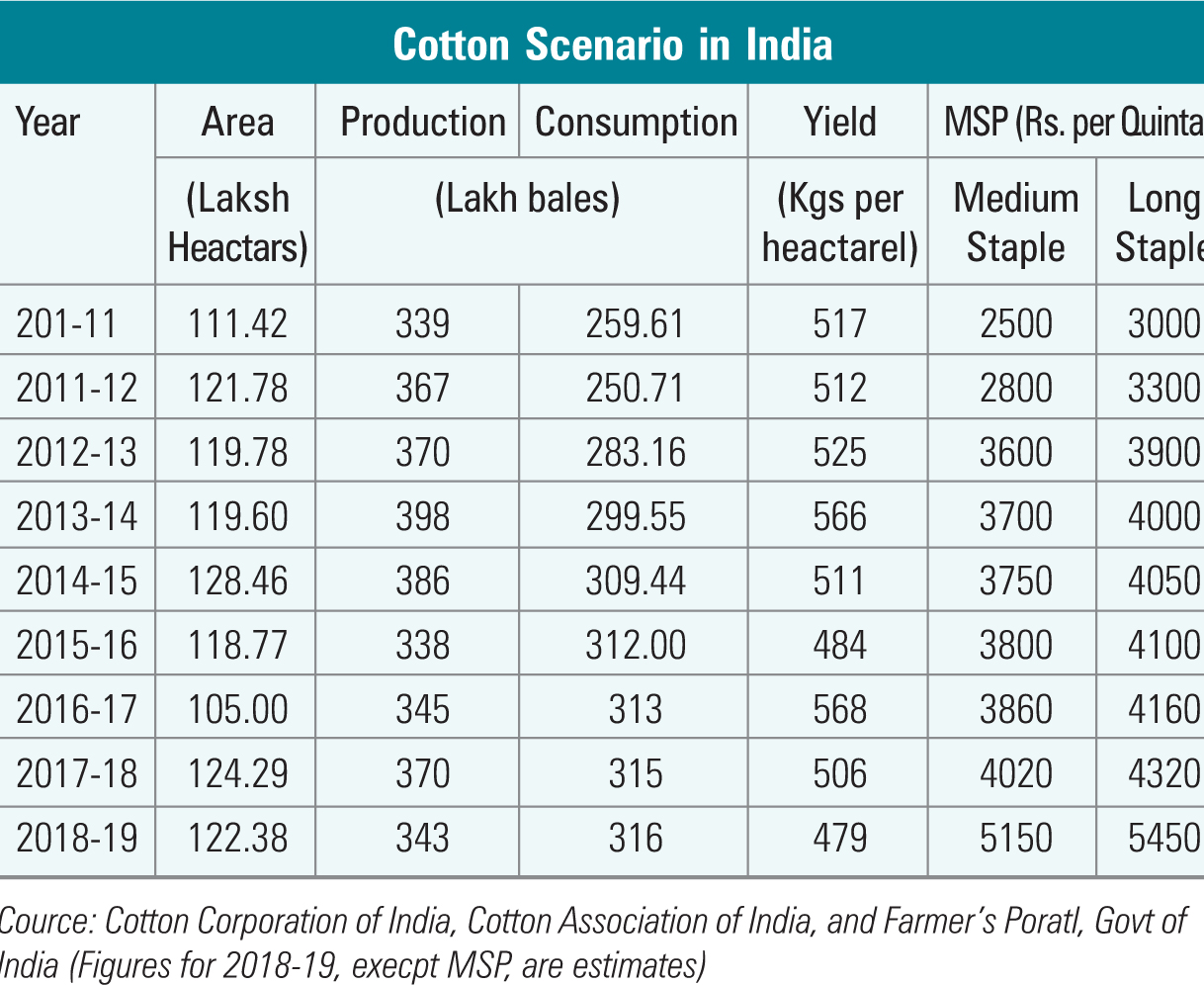

CITI Economic Desk notes that the area under cotton production in India has increased in the past few years with fluctuations throughout. Further, cotton yield has also been fluctuating as low as. 506 kg per hectare in 2017-18 as compared to other countries like China where it is more than 1700 kg per hectare.

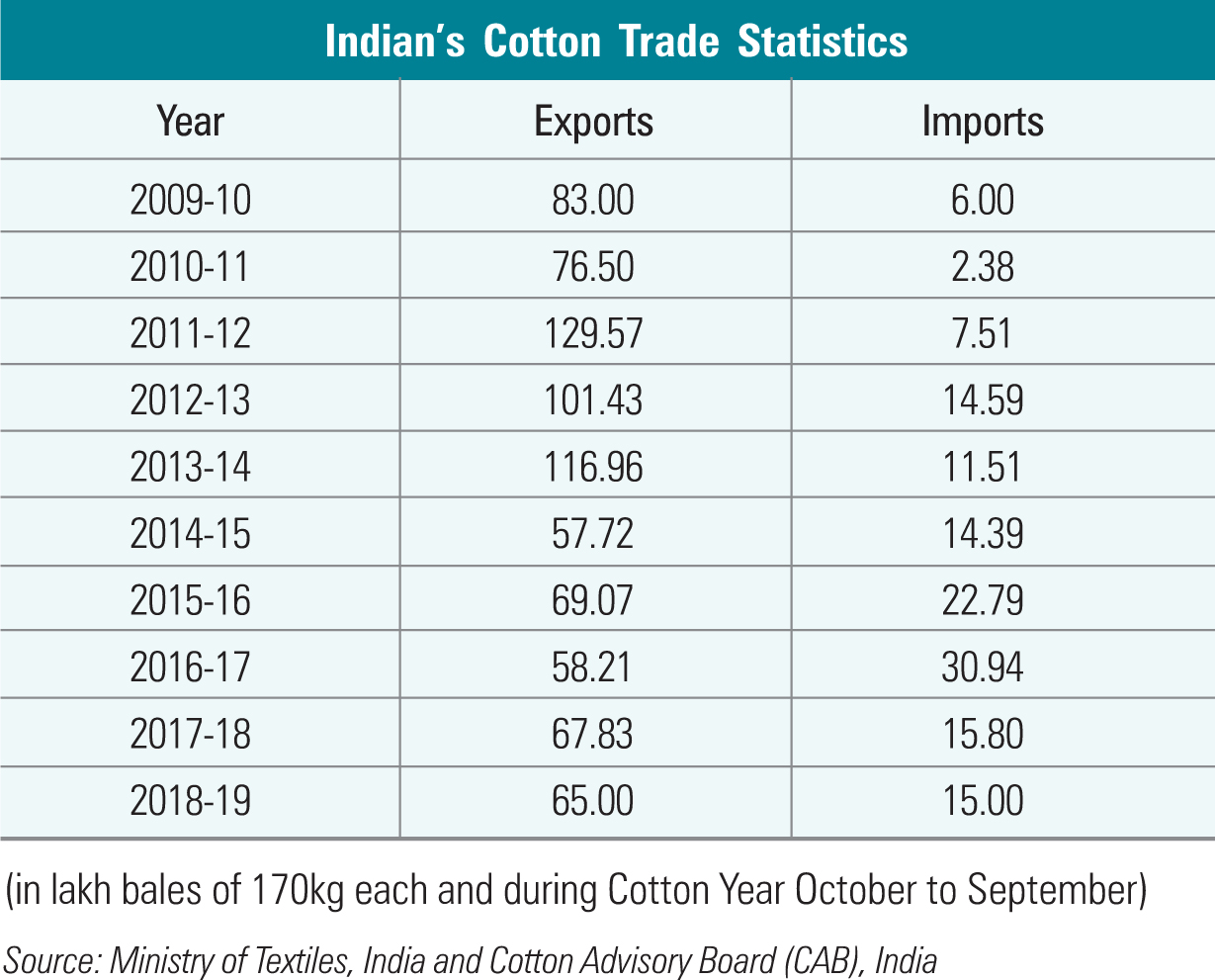

It was in 2014-15 that the highest cotton acreage was noticed (128.46 lakh hactares) in the last decade and highest cotton production was observed in 2013- 14 (398 lakh bales). Cotton yield has considerably declined during the last three years at a CAGR of almost 8.50 per cent from 568 per hectare in 2016-17 to 476 kg per hectare estimated in 2018-19. During the same period cotton exports have increased at a CAGR of almost 6 per cent from 58.21 lakh bales of 170 kg to 65 lakh bales of 170 kg, while imports have decreased.

It is known that cotton is the backbone of the textiles industry, which consumes around 59 per cent of the total fibre production, accounts for 34 per cent of exports, earning about `50,000 cr annually. Around 6 to 6.5 mn farmers grow cotton crop in about 11 States – Punjab, Haryana, Rajasthan, Gujarat Madhya Pradesh, Karnataka, Maharashtra, Andhra Pradesh, Telangana, Tamil Nadu and parts of Odisha. Around 60 mn people depend on growing cotton to eke out their living. Cotton is a raw material for 1500 mills (4 mn handlooms, 7 mn powerlooms and livelihood of 60 mn people. The textile and clothing industry contributes to about 14 per cent of industrial production and 4 per cent of GDP.

More than 80 per cent of cotton produced in the country is consumed locally and only about 17 per cent is exported, on an average, during the past three years. The textile sector consumes about 77 per cent of total cotton output, while the rest is used by non-textiles sector in products such as fishnets, bandages, swabs, book bindings etc.

India is the largest producer and the second largest exporters of cotton in the world, apart from being the second largest consumer. The rise in international trade and consequent integration of the domestic cotton market with the global market expose the domestic stake holders to global price fluctuations and the risks resulting from them. To safeguard against the risks arising from such price volatilities in cotton the first trading in futures contracts was introduces in the form of cotton futures on the Bombay Stock Exchange in 1875, after the first cotton futures was traded on the New York Cotton Exchange.

{kind=link}