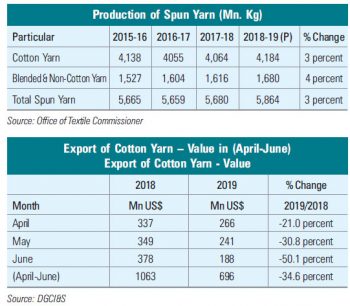

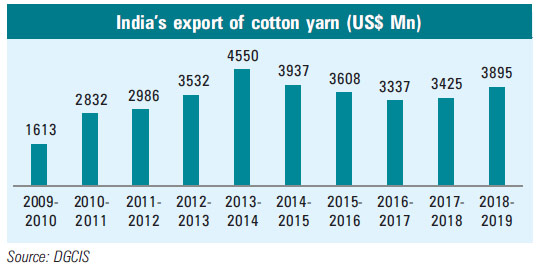

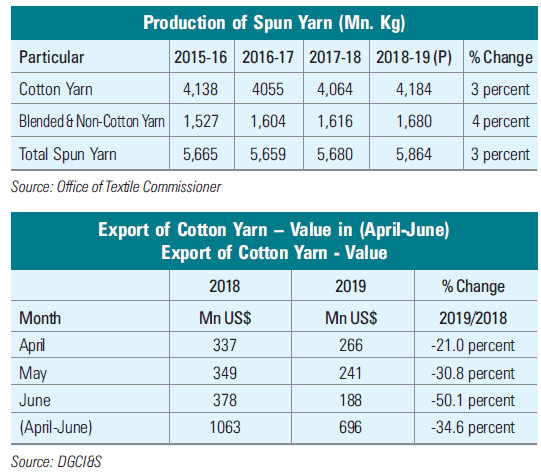

Besides, the sector is dogged by costly raw materials, cheaper imports of yarns and garments, inverted duty structure in the man-made fibre (NMF) textile industry value chain, exorbitant power cost due to cross subsidisation, interest rate etc., Raw materials, as in known, account for a major portion of the cost of production of any type of yarn. The raw materials include cotton and MMFs such as polyster staple fibre, viscose staple fibre and acrxlic staple fibre. The prevailing situation is aptly summed up by S.K. Khandelia, President and CEO, Sutlej Textiles and Industries Ltd thus “The spinning sector is pushed now to a non-performing one. It is caught in a web of heavy fall in yarn exports and subdued demand at home April – June 2019 exports fell by 34.5 percent to dollar 96 mn from dollar 1063 mn in the same period of 2018, leading to heavy job losses as well as financial losses. Khandelia has pinpointed cotton as the root cause of high fibre prices, which are costlier than international ones. Global cotton prices have plunged 28.3 percent in the past one year. In contrast, domestic prices have ruled firm in the same period on the back of a 28 percent increase in the minimum support price (MSP) for seed cotton (Kapas) Then the domestic prices of MMFs PSF, VSF etc are fixed on import parity basis. This means the landed cost of imported fibre carries customs duty, antidumping duty, ocean freight and these are included in the domestic prices, making it out of reach of textile mills. As a result, there has been on ever increasing imports of polyestor yarn, viscose yarn etc., adversely affecting the spinning industry and with costly raw materials, Indian textile products have been rendered uncompetitive in the global market.

Inspite of excess capacity, States have been encouraging establishment of new spinning units in their areas by offering attractive incentives. This has created problems for the existing units to compete with these domestic as well as export markets, further driving them into bankruptcy. Under the present dispensation, MMF attracts GST at 18 percent, yarn made out of that at 12 percent and fabrics at the rate of 5 percent. Refunds are allowed due to the inverted duty structures but it is cumbersome and time taking and results in blockage of funds. As has been reported in these columns earlier, there has been on increase in cheaper imports of garments from Bangladesh and Sri Lanka because of lower cost of their raw materials and other components. Apparel imports from Bangladesh grew 40. 47 per in April – June 2019 over the same period of the proceeding year. The 30 percent local value addition norm is being abused for import from third countries and routed via Bangladesh to take advantage of zero import duty. What with the sharp fall in demand and for yarn in China, our yarn exports have suffered due to disadvantage created by Free Trade Agreements (FTAs) of our competitors with big buying nations.

Inspite of excess capacity, States have been encouraging establishment of new spinning units in their areas by offering attractive incentives. This has created problems for the existing units to compete with these domestic as well as export markets, further driving them into bankruptcy. Under the present dispensation, MMF attracts GST at 18 percent, yarn made out of that at 12 percent and fabrics at the rate of 5 percent. Refunds are allowed due to the inverted duty structures but it is cumbersome and time taking and results in blockage of funds. As has been reported in these columns earlier, there has been on increase in cheaper imports of garments from Bangladesh and Sri Lanka because of lower cost of their raw materials and other components. Apparel imports from Bangladesh grew 40. 47 per in April – June 2019 over the same period of the proceeding year. The 30 percent local value addition norm is being abused for import from third countries and routed via Bangladesh to take advantage of zero import duty. What with the sharp fall in demand and for yarn in China, our yarn exports have suffered due to disadvantage created by Free Trade Agreements (FTAs) of our competitors with big buying nations.

Vietnam, Indonesia, Pakistan and Cambodia enjoy duty free access in China in different segments of cotton textiles, while Indian products bear 3.5 percent, 10 percent and 14 percent duty on yarn, fabrics and made-ups respectively. Demand for yarn can increase only if garments exports increase. Look at last years apparel exports. China exported $ 45 bn, Bangladesh $ 36 bn, Vietnam $ 33 bn and India a mere $ 17 bn. India is far behind China is steadily losing to smaller countries. Yarn is an intermediate product and therefore depends on the growth in consumption in down stream value chain like fabrics which has been very low. Indian textile and clothing exports have remained stagment since the last few years at $ 37-50 bn against $ 37.65 bn in 2014-15.

Vietnam, Indonesia, Pakistan and Cambodia enjoy duty free access in China in different segments of cotton textiles, while Indian products bear 3.5 percent, 10 percent and 14 percent duty on yarn, fabrics and made-ups respectively. Demand for yarn can increase only if garments exports increase. Look at last years apparel exports. China exported $ 45 bn, Bangladesh $ 36 bn, Vietnam $ 33 bn and India a mere $ 17 bn. India is far behind China is steadily losing to smaller countries. Yarn is an intermediate product and therefore depends on the growth in consumption in down stream value chain like fabrics which has been very low. Indian textile and clothing exports have remained stagment since the last few years at $ 37-50 bn against $ 37.65 bn in 2014-15.

Spinning mills are power intensive. The power cost works out to about 13 percent of the total production cost. State Governments have made open access of power prohibitive by levying very heavy cross subsidy surcharge and additional surcharge. On top is the heavy electricity duty. Khandalia also says that most spinning mills are cotton based. Only about 75 percent is of non-cotton yarn. The world trade has a share of more than 70 percent synthetic textiles and clothing and is increasing year after year. In India, however the share is only 28.30 percent. This is also one of the reasons for the stagnant T and C exports. Moreover the interest rate in India is high in general and for spinning mills in particular. Compared to other countries, this makes our textiles products uncompetitive in the global market. To make yarn exports competitive, all types of raw materials should be made available to the domestic

textile industry at international prices. Besides MMF should be customs duty free and anti-dumping duty free. This measure will help stop imports of unwanted MMF yarn like viscose yarn, polyester yarn etc., and also enable the spinning sector – which is cotton dominates – to diversify into the synthetics and emerge competitive at home and abroad. It will also lase the pressure on cotton yarn. In addition, the country will be able to export garments during all four seasons and garments units will be able to run to their full capacity throughout the year as globally cotton dominates spring and summer sales season and synthetics and blends dominate autumn and winter season. India will also be able to export sports wear fashion wear and such other garments which are synthetic based. To get cotton for the spinning units at world prices, determined by market forces of demand and supply, the government should pay the difference of MSP and market prices of seed cotton (kapas) to farmers by direct bank transfer.

To remove the inverted structure and to have a fibre neutral duty structure, it is strongly felt that the entire textile value chain, from fibre to garments, and for all types of fibres and blends thereof, should have the same rate of GST to avoid unnecessary complications and blockage of funds at different stages. This will also remove complications of getting refund on account of inverted duty structure. Refund is allowed for inverted duty so there will be no revenue loss to the government if the same GST rate is applied to the entire textile value chain.

The spinning sector, considered one of the important segments of the textile industry value chain, is left to fend for itself. What else can one say about the segment which has been struggling with surplus stock due to subdued demand at home and falling exports. The industry has no option but to cut back on production by about 15-30 percent to help keep inventory at a safe level. The government is not coming to the aid of the industry dispite several representations. There is no refund of Central and State taxes and levies under the Rebate of State and Central Taxes and Levies (ROSCTL) scheme. Cotton yarn is ineligible, while garments and made-ups receive refunds. This has only raised the cost of yarn exports eroding their competitiveness. The Merchandise Exports India Scheme (MEIS), introduced in 2014-15 is also not available to cotton yarn. The scheme should be extended to all types of spun yarn, cotton yarn bended yarn and 100 percent non cotton at 5 percent.

The spinning sector, considered one of the important segments of the textile industry value chain, is left to fend for itself. What else can one say about the segment which has been struggling with surplus stock due to subdued demand at home and falling exports. The industry has no option but to cut back on production by about 15-30 percent to help keep inventory at a safe level. The government is not coming to the aid of the industry dispite several representations. There is no refund of Central and State taxes and levies under the Rebate of State and Central Taxes and Levies (ROSCTL) scheme. Cotton yarn is ineligible, while garments and made-ups receive refunds. This has only raised the cost of yarn exports eroding their competitiveness. The Merchandise Exports India Scheme (MEIS), introduced in 2014-15 is also not available to cotton yarn. The scheme should be extended to all types of spun yarn, cotton yarn bended yarn and 100 percent non cotton at 5 percent.

{kind=link}