Which country is able to take advantage of China’s lower than market performance in apparel exports with its share expected to come down from 41 percent currently to 35 percent by 2025?

The beneficiary nations of this opportunity would be those that have competitive manufacturing cost, FTA advantage with markets and global infrastructure.

India is better placed to take advantage of the situation. But it has not yet fully tapped the real potential of its apparel exports and its fortunes will all depend on early finalisation of an FTA with EU. Negotiations are on at present. Apart from this, conversion of this potential into reality will call for tremendous structural changes in policy framework-from refining of labour laws to exit policies, among other bottlenecks, recommends a report prepared by Wazir Brothers.

The report titled “The Road to 2025” notes that despite slowdown in its apparel exports in China with vast land base, plentiful resources, manpower strength and large manufacturing setup will continue to be the single largest apparel global manufacturer in the foreseeable future. The slowdown will continue till its domestic market becomes increasingly attractive for local manufacturing.

At the same time it has to be recognized that China is longer a low cost destination with shrinking labour pool and reduced flow of migrants from rural areas. Wages across sectors and regions have grown in double digits in the last couple of years and will continue to grow further. This can put a break on fast growth of manufacturing recorded historically.

Conventional textiles and apparel industry will no longer be the prime focus of Chinese Government as it has been since 1990’s. Chinese enterprises will concentrate more on innovation driven industries like aerospace, artificial intelligence etc. China has established trade pacts with several South East and East Asian countries where manufacturing costs are lower than China where it will invest and support manufacturing to cater to domestic demand and exports.

For India, it also needs to develop textile capability and scale of manufacturing comparable to that of China. Added advantage is FTA’s with US as well. Here the report made a pertinent point. China has survived without FTA’s. None of the five garment suppliers to the US-China, Vietnam, Bangladesh, India and Indonesia have any preferential access to US.

India’s production of textiles is diversified while for others apparel exports are the backbone of their economies. India is the only country which has the “wherewithal to take up every single dollar spillover from China because of its vast manpower availability and infrastructure.” the report points out. However, like China, its own domestic market is getting increasingly attractive.

Exports had played an important role in China’s economic success. But now China is at a juncture where private consumption is replacing investment as a major driver of GDP growth and eventually constitutes the largest share of GDP. High levels of investment are converting into consumption creating structural changes in the export oriented sectors like apparel.

Source: IMF’s World Economic Outlook Database, Oct. 2015; UN’s World Population Prospects: The 2015 Revision; and GDP projections 2016 onwards based on Real GDP growth rate database published by Economic Research Service, USDA, last updated Dec. 2015

Between 2001 and 2004, the report says Chinese apparel exports increased more than fivefold from $30 billion to $170 bn, growing at 14 percent CAGR. After 2010, exports had slowed down compared to the period before financial crisis where annual growth was 20 percent on an average. The trend is expected to remain in the same in future.

The report further notes that the demand for apparel in China is slated for higher growth per capita spending on apparel is expected to rise from dollar 171 billion in 2015 to dollar 434 billion by 2025. Addition of dollar 77 billion in the domestic market will exert pressure on exports and will result in higher imports.

China and India have received most attention from international companies in recent times with their huge population and growing economies. India had replaced China as the largest recipient of foreign domestic investment (FDI) in 2015. Macro-economic projections show continuation of high growth in both countries leading to doubling of GDP by 2025.

Both Chinese and Indian markets have shown robust growth in the past despite global uncertainties and slack demand. From 2007 and 2025, the Chinese market had posted on annualised growth of 15 percent whereas Indian market registered a somewhat lower growth of 11 percent.

However both the markets have performed better than the US, Japan, and EU, the largest consumption regions where change in economic conditions led to lower demand growth. In both China and India demand for clothing is expected to outweigh economic growth.

It is projected that China’s per capita expenditure on apparel will rise from dollar 177 billion in 2015 to dollar 434 billion by 2025, a CAGR growth of 10 percent. India’s per capita expenditure on apparel will increase from $45bn to $180 billion in this period.

Whereas these two economies will drive the growth of global apparel consumption, the traditional markets of US and EU will witness slower growth rates due to market maturity and weaker growth. By 2025, the combined size of Indian and Chinese markets will overtake that of US and EU.

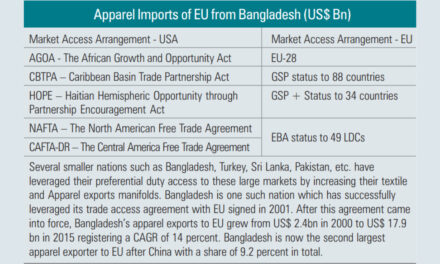

According to the report, textiles and apparel are price sensitive commodities. As textile and apparel manufacturing is a labour intensive industry several countries adopt a protected regime by imposing high import duties to safeguard the interest of domestic industry. Therefore FTA’s have a special role to play in the development of investment and trade in this sector.

Key apparel markets-EU, US and Japan-have multiple market access arrangements with several key manufacturing nations. They have entered different types of trade agreements. These include Economic Partnership Agreement, Economic Cooperation Agreement, Customs Union, Economic Union, FTAs, and PTAs or provided special status (GSP, GSP + EBA) to certain countries thereby lowering or eliminating tariff rates.

Bangladesh, Turkey, Sri Lanka, Pakistan etc. have emerged as a major apparel exporters mainly because of preferential duty access they have to one or more of these markets.

In fact China is the only large manufacturer of textiles and apparel which does not have any special market access to the US, EU or Japan.

Bangladesh’s apparel exports to EU were Euro 2-6 billion which reached Euro 13.7 billion in 2015, growing at CGAR of 12 percent. It has become the second largest exporter of apparel in EU after China.

Also there are examples where countries could not take the benefit of duty free access. For instance, sub Saharan African nations (SSA) have preferential market access to US under African Grown Opportunities Act (AGOA) with relaxed Rules of Origin (ROO) for apparel under third country fabric clause. Data however reveals that US imports of textiles and apparel under AGOA rose initially till 2004 but declined thereafter.

Only three SSA nations-Kenya, Lestho, Mauritius-have taken advantage offered by AGOA to any appreciable extent so far. But even then their share of textiles and apparel exports to the US market is insignificant.

{kind=link}