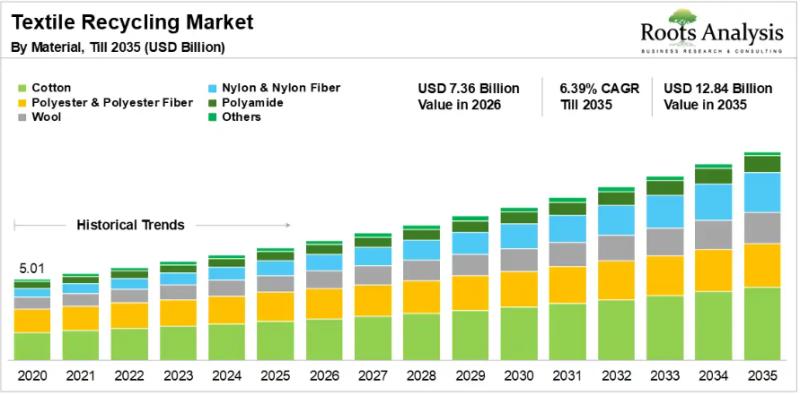

The global textile recycling market, valued at USD 5.01 billion in 2025, will expand to USD 7.36 billion in 2026 and reach USD 12.84 billion by 2035, advancing at a CAGR of 6.39% over the forecast period. The market’s trajectory reflects mounting pressure on fashion and manufacturing industries to redirect billions of kilograms of discarded textiles away from landfills and toward productive, circular use. For investors, brands, and policymakers, the growth math is straightforward: regulatory mandates are tightening globally, consumer expectations around sustainability are rising, and the economics of recycled fiber are improving as technology scales.

The global textile recycling market, valued at USD 5.01 billion in 2025, will expand to USD 7.36 billion in 2026 and reach USD 12.84 billion by 2035, advancing at a CAGR of 6.39% over the forecast period. The market’s trajectory reflects mounting pressure on fashion and manufacturing industries to redirect billions of kilograms of discarded textiles away from landfills and toward productive, circular use. For investors, brands, and policymakers, the growth math is straightforward: regulatory mandates are tightening globally, consumer expectations around sustainability are rising, and the economics of recycled fiber are improving as technology scales.

MARKET OVERVIEW

Textile recycling encompasses the recovery of fibers, yarns, and fabrics from discarded garments and industrial textile waste, then reprocessing those materials into new products. The scope runs well beyond clothing. Recycled fibers serve automotive interiors, sound and thermal insulation, nonwoven composites, construction materials, and agricultural packaging, making the textile recycling industry a supply chain input for multiple sectors simultaneously.

Two forces are converging to make this a high-growth space right now. First, the sheer scale of textile waste is no longer manageable through conventional disposal. Fast fashion cycles have compressed garment lifespans while production volumes keep rising, generating quantities of post-consumer waste that landfill capacity cannot absorb indefinitely. Second, regulatory frameworks in Europe, North America, and Asia-Pacific are shifting the cost of that waste from municipalities onto the brands that created it. Extended Producer Responsibility laws are making recycling infrastructure investment an operational necessity, not a corporate social responsibility gesture.

Industry activity confirms the momentum. In March 2025, PUMA and RE&UP announced a multi-year collaboration to transform textile waste into recycled cotton fibers and polyester chips, with PUMA targeting 30% fiber-to-fiber recycled polyester in its apparel by 2030. In October 2025, plastics recycling equipment leader Erema acquired a stake in BlockTexx, a Brisbane-based startup, to advance textile-to-textile recycling at industrial scale. Swedish recycler Syre secured supply partnerships with Gap and Target in June 2025 to provide recycled polyester as demand for sustainable fashion grows.

KEY GROWTH DRIVERS

Landfill Pressure and Fast Fashion Waste Volumes Rapid growth in global textile consumption, driven by fast fashion and shorter garment lifecycles, has generated textile waste quantities that governments and NGOs can no longer absorb through traditional disposal methods. This volume pressure creates the raw material pipeline that makes recycling economically viable and gives the industry a reliable feedstock base.

Regulatory Mandates and Extended Producer Responsibility The EU now requires separate textile waste collection systems, and multiple states in the U.S. have enacted textile waste bans aligned with 2030 reduction goals. These frameworks compel brands and manufacturers to take direct responsibility for end-of-life textiles, incentivizing investment in reuse, upcycling, and sustainable material sourcing across the supply chain.

Advances in Chemical and Automated Sorting Technologies Chemical recycling innovations now allow high-quality fiber recovery from blended textiles that mechanical processes cannot handle. Separately, AI-driven sorting systems and robotics are improving throughput, reducing contamination in recycled batches, and lowering operational costs. In September 2025, Samsara Eco opened a commercial textile recycling plant using AI-engineered enzymes, a concrete example of this technological progression reaching commercial scale.

Rising Corporate Sustainability Commitments Major apparel brands are embedding recycled fiber targets into their supply chain strategies, creating stable demand for recycled polyester, cotton, and blended outputs. These commitments, often anchored to 2030 or 2035 sustainability goals, translate into long-term offtake agreements that reduce commercial risk for recycling operators and attract capital to the sector.

Expansion of Take-Back Programs and Collection Infrastructure Incentivized take-back schemes are expanding the supply of recyclable post-consumer material. As collection rates increase, recycling facilities can operate at greater capacity, improving unit economics and making the business case for new plant investment. This infrastructure development is particularly active in Germany, France, and Italy, which already anchor Europe’s leading collection network.

MARKET SEGMENTATION

The textile recycling market segments by type of material (cotton, polyester, nylon, polyamide, wool, and others), form (fabrics, fibers, yarns), source (apparel waste, automotive waste, home furnishing waste), type of textile waste (post-consumer and pre-consumer), recycling process, distribution channel, and end use industry. The mechanical recycling process currently dominates, holding a 73.73% share of overall revenue. Its advantages are straightforward: lower operational costs, established processing technology, and the ability to handle a wide variety of natural and synthetic fibers without complex chemical inputs.

The chemical recycling sub-segment, however, is on the fastest growth trajectory within the recycling process category. It addresses the significant limitation of mechanical methods, which struggle with blended fabrics, by enabling better fiber recovery from complex mixed-material textiles. Stricter environmental regulations are accelerating adoption. By end use, the apparel sub-segment commands the largest share at 46.60%, driven by both the highest volume of textile waste generation and the fashion industry’s accelerating shift toward circular sourcing models.

REGIONAL INSIGHTS

Europe leads the global textile recycling market with a 29.67% share, a position built on stringent environmental regulation, established recycling infrastructure, and strong circular economy policy frameworks. Germany, France, and Italy account for a significant portion of that leadership, supported by high waste collection rates, public awareness programs, and the presence of major recycling operators and sustainable fashion brands within the region. The EU’s mandate for separate textile waste collection systems, effective from 2025, is strengthening this foundation further.

Asia-Pacific is the fastest-growing region globally, propelled by large textile manufacturing hubs in China, India, and Vietnam, rising policy support for sustainability, and growing corporate investment in recycling capacity. Vietnam’s Binh Dinh province signed a memorandum of understanding with Sweden’s Syre Group in June 2025 for a polyester fabric recycling project, an early signal of the foreign investment flowing into the region’s recycling infrastructure. North America is also active, with state-level textile waste bans and brand-driven take-back programs building momentum, particularly in the northeastern United States.

COMPETITIVE LANDSCAPE

Key players profiled in the textile recycling market report include Lenzing AG, Aditya Birla Group (Birla Cellulose), Evrnu, Carbios, Syre, Unifi, Worn Again Technologies, Infinited Fiber Company, Recover Textile Systems, Circ, Ambercycle, REMONDIS, Leigh Fibers, Martex Fiber, Boer, and Patagonia, among others.

The competitive structure combines established fiber producers with a wave of technology-focused startups, each competing on the strength of proprietary recycling processes rather than pure scale. Lenzing AG leads through high-volume sustainable fiber production serving multiple end-use industries, while Aditya Birla Group advances closed-loop and fiber-to-fiber systems through its Birla Cellulose brand. Startups such as Evrnu, which uses patented fiber regeneration to convert discarded garments into high-performance recycled fibers, and Carbios, which applies enzymatic processes to polyester recovery, are attracting strategic partnerships with major brands eager to meet their 2030 sourcing targets. The primary competitive battleground is technology differentiation, specifically the ability to process blended and contaminated textile waste at industrial scale with output quality that meets apparel-grade fiber standards.

Source: https://www.openpr.com

{kind=link}